Cash Flow Is King: The Restaurant Owner's Survival Guide to Never Running Out of Money

Profitable restaurants go bankrupt every year because they run out of cash. Master the cash flow strategies that keep your doors open and your suppliers paid — even during slow months.

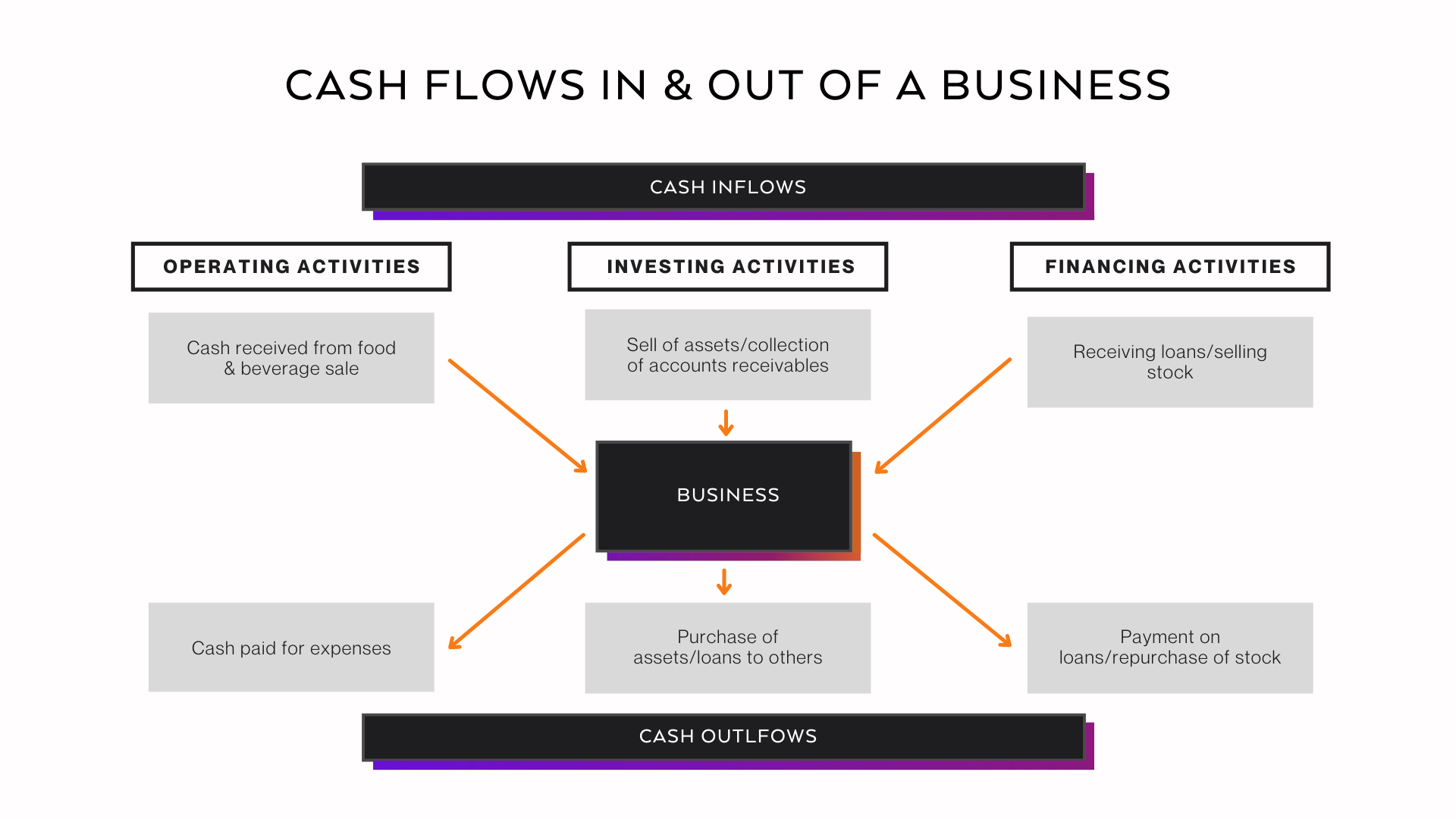

Here's a paradox that confuses a lot of new restaurant owners: you can be profitable on paper and still go bankrupt.

I know because I've watched it happen. A bistro owner in Austin showed me his year-end P&L — $82,000 net profit. He should have been celebrating. Instead, he was three weeks from closing because he couldn't make payroll.

How? His profit existed in accounts receivable, inventory, and a tax bill he hadn't set aside for. His bank account had $4,200 in it.

Profit is an accounting concept. Cash is survival. And if you don't learn to manage cash flow from day one, all the great food and five-star reviews in the world won't save you.

Let me teach you what I teach every restaurant owner I work with.

Understanding Restaurant Cash Flow

Why Restaurants Are Uniquely Vulnerable

Restaurants have a cash flow profile unlike almost any other business:

| Cash Flow Challenge | Why It's Unique |

|---|---|

| Daily revenue collection | Cash comes in daily but bills are monthly |

| Perishable inventory | You can't "save" unsold food for next month |

| Fixed costs are enormous | Rent, insurance, and loan payments don't flex with slow weeks |

| Seasonal swings | January revenue might be 40% of December revenue |

| Labor can't be instantly adjusted | You can't send people home when it's slow (well, you can, but you'll lose them) |

| Supplier payment terms are short | Food suppliers typically want Net 7 or Net 14, not Net 30 |

This means you can have a great month followed by a terrible month and the terrible month's bills still need to be paid — with cash you may have already spent.

The Weekly Cash Flow Tracking System

Monthly financial reviews aren't enough for restaurants. You need weekly visibility into your cash position.

The Friday Cash Flow Check (30 Minutes That Save Your Business)

Every Friday, update this simple tracker:

| Line Item | This Week | Next Week (Projected) | Week After |

|---|---|---|---|

| Starting cash balance | $XX,XXX | ||

| + Revenue collected | |||

| - Payroll | |||

| - Food/beverage invoices due | |||

| - Rent/occupancy | |||

| - Utilities | |||

| - Loan payments | |||

| - Other obligations | |||

| = Ending cash balance |

Cash Flow Red Flags

Take immediate action if:

- Cash balance drops below 2 weeks of operating expenses

- You're choosing which bills to pay (this is called "juggling" and it ends badly)

- You're relying on this weekend's sales to cover this week's payroll

- Credit card processing deposits are your only source of cash

The Cash Reserve Strategy

How Much Cash Should You Have?

I recommend every restaurant maintain a cash reserve equal to 4-6 weeks of total operating expenses. This isn't profit — it's your safety net.

| Monthly Operating Expenses | Minimum Reserve (4 weeks) | Ideal Reserve (6 weeks) |

|---|---|---|

| $30,000 | $30,000 | $45,000 |

| $50,000 | $50,000 | $75,000 |

| $75,000 | $75,000 | $112,500 |

| $100,000 | $100,000 | $150,000 |

Building the Reserve

If you don't have this reserve (most new restaurants don't), build it systematically:

For a restaurant doing $20,000/week in sales, 2.5% is $500/week. In one year, that's $26,000 — which could be the difference between surviving a slow January and closing permanently.

Free: Restaurant Finance Cheat Sheet

Master your numbers with our cheat sheet covering food cost formulas, break-even analysis, and cash flow templates.

No spam, ever. Unsubscribe anytime.

Managing Seasonal Cash Flow Swings

The Annual Cash Flow Map

Every market is different, but most restaurants experience predictable patterns:

| Period | Typical Pattern | Cash Flow Impact |

|---|---|---|

| January-February | Slowest months, post-holiday drop | ⚠️ Negative cash flow likely |

| March-April | Gradual recovery, spring events | 🔄 Break-even to slight positive |

| May-June | Summer ramp-up, patio season | ✅ Positive cash flow |

| July-August | Vacation season (varies by market) | ✅ Generally positive |

| September-October | Strong fall season, back-to-school | ✅ Positive cash flow |

| November-December | Holiday parties, gift cards, events | ✅✅ Peak cash flow |

The Seasonal Cash Flow Playbook

During peak months (Oct-Dec):

- Aggressively build your cash reserve

- Prepay suppliers for discounts if offered

- Stock up on non-perishable supplies at current prices

- DO NOT increase fixed costs (don't sign a bigger lease, don't buy new equipment on credit)

- Reduce labor hours strategically (but don't cut so deep that you lose good people)

- Run promotions that drive traffic without heavy discounting (e.g., prix fixe menus, cooking classes)

- Negotiate extended payment terms with suppliers

- Focus on marketing for catering, private events, and gift card redemption

The Vendor Payment Strategy

Optimizing When You Pay

Your payment timing directly impacts cash flow. Here's how smart operators manage it:

Prioritize payments in this order:

Negotiating Better Terms

- Ask your top 3 suppliers for Net 21 or Net 30 terms instead of COD or Net 7

- Offer a larger volume commitment in exchange for longer payment terms

- Consider credit cards for purchases — you get 25-30 days of float (just pay the balance in full)

- Explore restaurant-specific lines of credit as emergency backup (apply when you don't need it)

Gift Cards: Your Secret Cash Flow Weapon

Gift cards are one of the most underutilized cash flow tools in the restaurant industry.

Why Gift Cards Are Cash Flow Gold

Maximizing Gift Card Sales

- Offer a bonus incentive during holidays: "Buy $100, get a $20 bonus card"

- Sell them at the host stand, on your website, and through social media

- Train servers to mention them as departure: "Gift cards are available if you'd like to share the experience"

- Track redemption patterns to forecast the cash flow benefit accurately

Emergency Cash Flow Tactics

Sometimes, despite your best planning, cash gets tight. Here's your emergency playbook:

Tier 1: Mild Cash Crunch (2-3 weeks tight)

- Delay non-essential purchases (new smallwares, décor updates)

- Run a flash promotion to drive immediate traffic

- Push gift card sales aggressively

- Request 7-day extensions on upcoming vendor payments

Tier 2: Serious Cash Crunch (can't cover next payroll)

- Have an honest conversation with your landlord about a short-term deferral

- Access your line of credit (this is exactly what it's for)

- Consider a merchant cash advance as absolute last resort (the rates are brutal, but it's fast)

- Cut all discretionary spending immediately

Tier 3: Crisis (multiple obligations at risk)

- Engage a restaurant financial consultant or accountant immediately

- Explore SBA disaster loans or emergency funding

- Have honest conversations with your key suppliers — they'd rather work with you than lose a customer

- Evaluate whether operational changes (reduced hours, temporary menu reduction) can stop the bleeding

The Tax Trap: Set It Aside or Pay the Price

This catches more first-time owners than almost anything else: sales tax and payroll tax are not your money.

You collect them, you hold them temporarily, but they belong to the government. The moment you spend tax money on operations, you're borrowing at the worst possible interest rate — with penalties, interest, and potential criminal liability.

My non-negotiable rule: Open a separate account for tax obligations. Transfer payroll tax every pay period and sales tax every week. Never, ever "borrow" from it.

Building Long-Term Financial Health

Once you survive the first year, shift your focus from survival to building a financially resilient operation:

The restaurants that last decades — the legendary places we all admire — they're not just great at food. They're great at money.

And you can be too. It just takes discipline, visibility, and the willingness to look at the numbers even when they're uncomfortable.

Start building your financial plan with our [Startup Cost Calculator](/tools/startup-cost) and [Break-Even Analysis](/tools/break-even). Our [Financial Projections Tool](/tools/financial-projections) can help you map cash flow across your first year.

Tags

Recommended Tools

Put This Knowledge Into Action

Use these tools to apply what you just learned